Property funds have become a popular way to gain exposure to real assets without the complexity of direct ownership. They can provide consistent income, diversification, and long-term capital growth. Yet, as with all investments, they carry risks.

For investors, whether seasoned professionals or families seeking to build wealth safely, understanding how to assess these risks is every bit as important as considering the potential returns. A property fund that is carefully structured and well managed can protect capital and deliver peace of mind. One that is poorly managed can expose investors to unnecessary uncertainty.

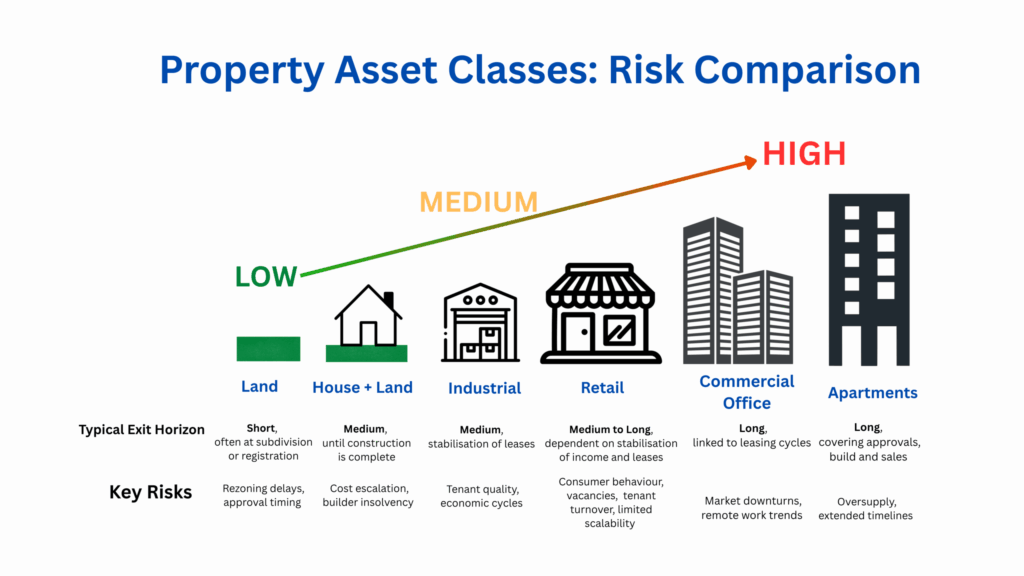

Understanding the Underlying Asset

The starting point for any risk assessment is the type of property that the fund is investing in. Different asset types carry very different levels of risk and reward.

- Land-only funds are generally the safest. These focus on subdividing and registering land, avoiding the risks of construction. They usually have shorter exit horizons and more predictable outcomes.

- House and land packages involve additional exposure once construction begins. The demand is usually strong, but the risk of cost overrun, delays and builder insolvency must be considered.

- Townhouses and apartments can offer higher returns but carry approval risk, longer build times and potential oversupply in certain markets.

- Industrial property, such as warehouses and logistics hubs, is in demand due to e-commerce. These assets can generate reliable income, though they depend on tenant stability and broader economic conditions.

- Retail centers can be attractive for steady income but are vulnerable to changes in consumer behaviour. Smaller retail strips and convenience centres may be more resilient, but they are not immune to tenant turnover.

- Commercial office buildings can perform strongly, but they are exposed to interest rate changes, economic cycles, and the evolving nature of how people work.

A critical risk factor is whether the project has approvals. A site with a Development Approval or planning permit in place is less risky than one waiting for approval. If it has progressed further with a Construction Certificate or building permit, even more uncertainty is removed.

Location also matters greatly. Land in growth corridors, supported by population growth and infrastructure investment, generally offer more resilience than speculative sites in regional areas.

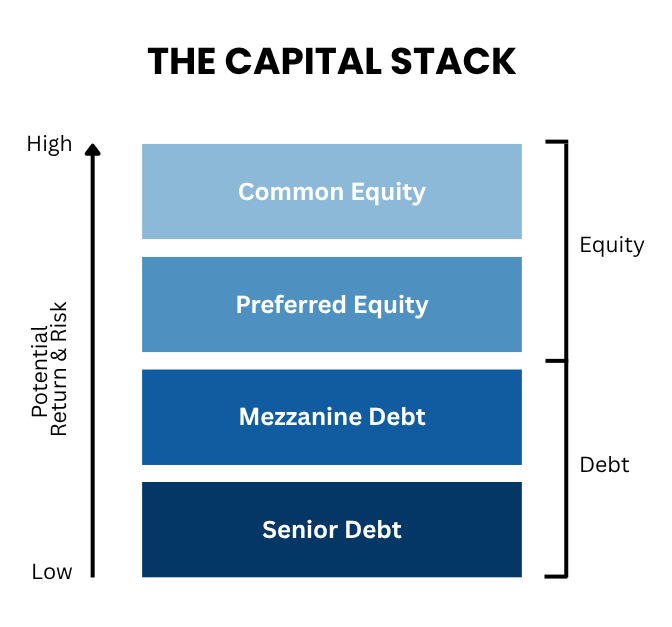

The Structure of the Fund

- Senior debt funds provide secure, fixed returns but are rare outside specialised institutions.

- Preferred equity funds sit between debt and common equity. They often provide better returns than debt with some downside protection.

- Growth or common equity funds involve the most risk and the longest timeframes but also the potential for the highest upside.

Exit flexibility is just as important as return. Investors should look carefully at how long their capital will be tied up and whether there are opportunities to redeem earlier. Funds with shorter timeframes or interim exit points provide an added layer of comfort.

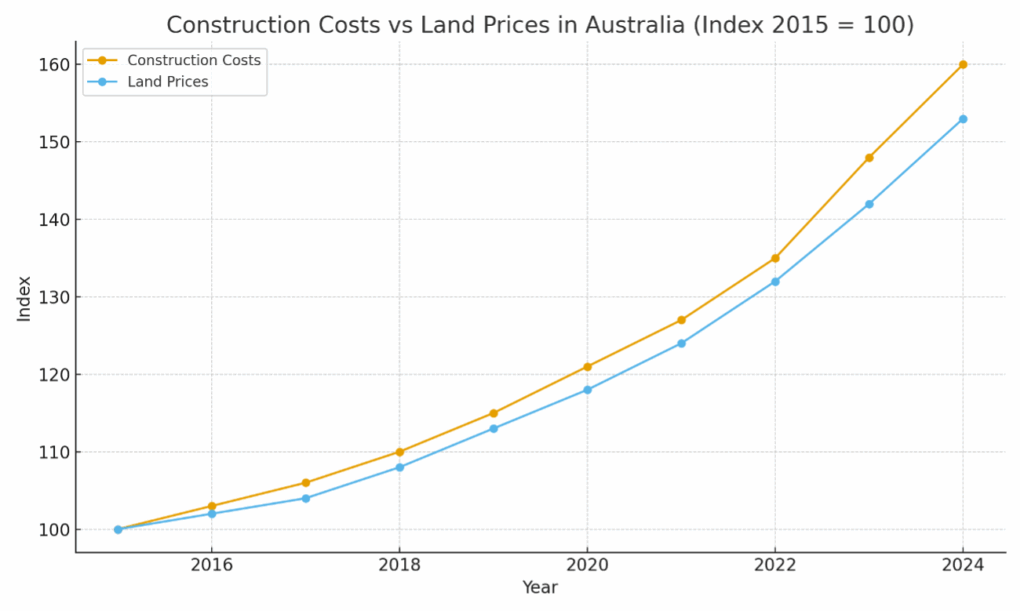

The Pressure of Construction Costs

When a property fund involves any form of building, one of the most important risks to understand is construction cost escalation.

In Australia, the cost of building has risen sharply in recent years. Material shortages, rising wages for skilled trades, new regulatory requirements and supply chain issues have all contributed. According to the Australian Bureau of Statistics, construction output prices rose by more than ten per cent in some recent years, with detached housing costs jumping as much as fifteen per cent.

By comparison, land prices have also risen steadily, but their growth has been more consistent and less volatile.

The chart below illustrates this point, showing how both construction costs and land prices have been appreciated over the past decade. While land has followed a steady upward path, the cost of building has accelerated at a sharper rate, creating a significant risk for projects that involve construction.

For investors, this means that funds exposed to construction must be examined with care. Key questions include whether the developer has locked in prices with builders, whether there is sufficient contingency built into the budget, and whether the structure of the fund protects investors if costs overrun.