Real estate private credit, as an asset class, is inherently risky.

Defaults, delays and aggressive valuations are a natural part of the landscape, and that is precisely why the returns are attractive.

But risk and recklessness are not the same thing.

In this article, we break down how FivePearls navigates these risks to continuously deliver strong risk adjusted returns for our investors.

1) Asset Class Risks

Construction Costs and Project Delays:

Vertical construction—particularly medium- and high-density apartment projects—is under unprecedented pressure. Complex engineering, multi-year build timelines, and a structurally undersupplied labour market significantly increase the probability of cost overruns. Even minor issues, such as engineering oversights, material shipment delays, or small scheduling disruptions, can extend timelines and compound financing costs, turning a profitable project into a loss-making one before the structure is complete.

Pre-Sales:

Apartment developers are often required to lock in prices years in advance through extensive pre-sales. In a market with sustained property price growth, this can mean forfeiting meaningful upside that could have been captured by selling at completion.

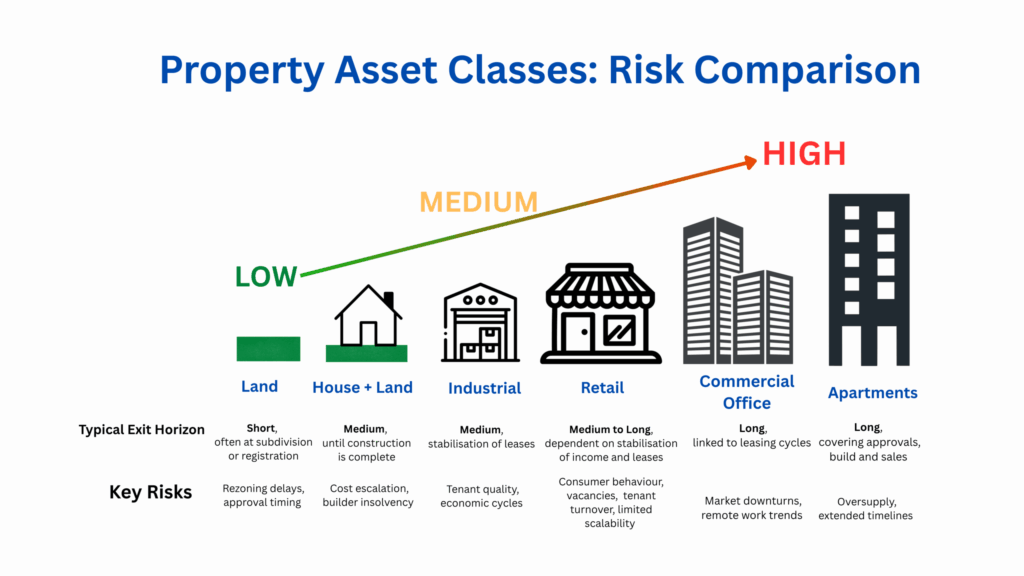

| Apartment | Land Subdivision |

Development Cost per Dwelling | >$350,000 | $140-170,000 |

Typical Construction Timeframe | 24-36 months | 12-18 months |

For private investors, the challenge is gaining exposure to these markets without having to buy and manage property directly, which is why more are gravitating toward property funds as a strategic entry point.

Source: www.productivity.nsw.gov.au

Mitigation: Avoid vertical construction risk.

By focusing exclusively on “horizontal” land subdivision, we avoid many of the variable risks inherent in vertical building. Civil works (roads, drainage, and utilities) are generally more predictable, more standardised, and delivered in a shorter timeframe. Land developers can also stage lot releases, effectively drip-feeding supply, allowing them to capture upside progressively as each stage is released.

Mitigation: Choose the right developer.

A developer with a proven track record, specifically within the same Local Government Area (LGA), often has intangible “planning alpha.” They understand local council processes and common friction points, which are frequently the primary drivers of approval and delivery delays. We prioritise developers who have consistently demonstrated the ability to move from DA approval to titled lots with high execution efficiency.

2) Location Risk

Regional or sub-prime markets often lack the deep, consistent buyer pools seen in major capitals. Weak or inconsistent demand directly reduces the absorption rate. A project expected to sell out in 12 months may take 36 months, causing holding costs to escalate and materially eroding profitability

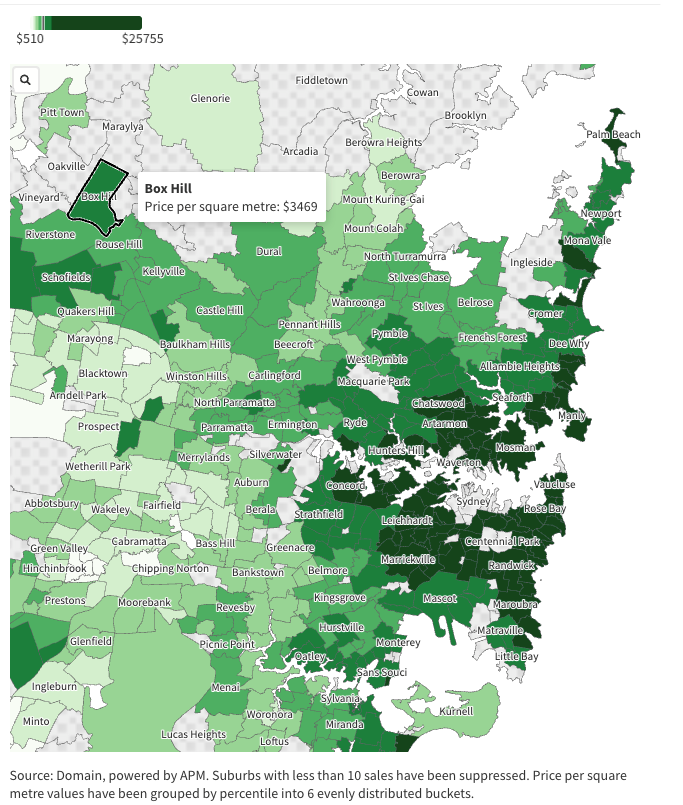

Mitigation: Avoid sub-prime and non-urban markets; focus on Sydney only.

Sydney land benefits from structural scarcity and strong population growth. It is more than 50% more expensive than Melbourne and roughly double the price levels of Brisbane, Adelaide, or Perth.

Land, even in the suburban outskirts of Sydney such as Box Hill, can command prices of ~$3,500 per square meter; over $1,000,000 for a 300 square meter parcel of land.

Persistent demand paired with constrained supply supports stronger sales velocity, reducing the risk of prolonged absorption and extended holding periods.

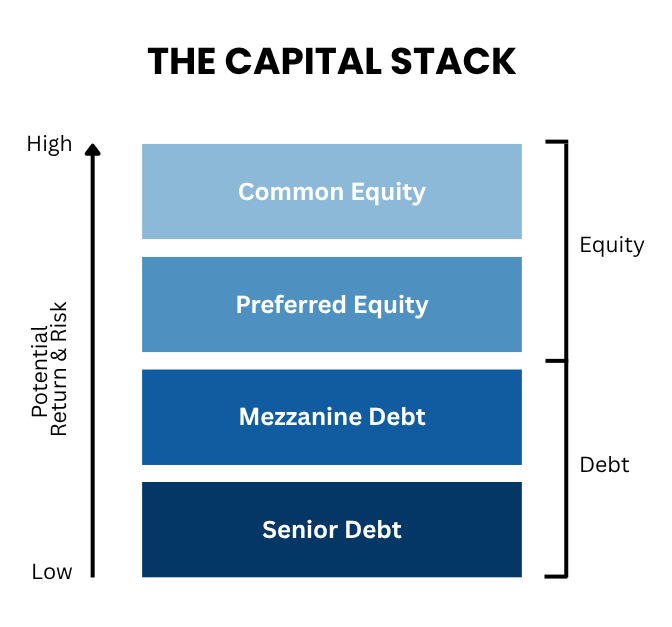

3) Credit Risk

In a subordinated debt structure where returns are higher, but the investment ranks behind a senior lender, the margin for error in security assessment is minimal. The most critical discipline in private credit risk management is valuation methodology. Some lenders underwrite against “as-if-complete” basis, which relies on optimistic assumptions and can obscure downside risk.

Mitigation: Use extremely conservative LVR and “as-is” valuation

After comparing 3 years of independent valuations, we lend against security on the most conservative “as-is” valuation, maintaining a minimum 50% loan-to-value ratio (LVR). The advantage of working with large-scale, well-capitalised developers is balance sheet depth. Rather than relying solely on security over the project site, we may also take security over other land assets owned by the developer. By utilising these assets as additional collateral, repayment capacity is supported by tangible, current land value, not solely by successful project completion.

CBRE forecasts the size of Australia’s real estate private credit sector to increase from $50bn currently to $90bn by 2029.

Real estate private credit offers a compelling return premium, but it is not an asset class that rewards a passive approach. The risks are real, varied, and demand constant attention. Developer defaults, builder insolvencies, and aggressive valuations do not manage themselves.

This is why the quality and integrity of your fund manager matters as much as the opportunity itself. A disciplined manager with a rigorous underwriting process and a genuine commitment to investor outcomes is a necessity. At FivePearls, that responsibility sits at the core of everything we do. Across all of our funds, we have maintained zero loss of capital and zero loss of stipulated returns for our investors.

Not by avoiding the complexity of this asset class, but by navigating it with the care and discipline it demands.